News Releases

15_08_22

Computable Contracts – A vision of the future

The London Market recently took another important step forward towards a digital future. Earlier this year, the London Market Group’s Data Council approved the commencement of a consultation process on the changes to the Market Reform Contract (MRC) to create the Intelligent Market Reform Contract (iMRC).

What on earth does that mean?

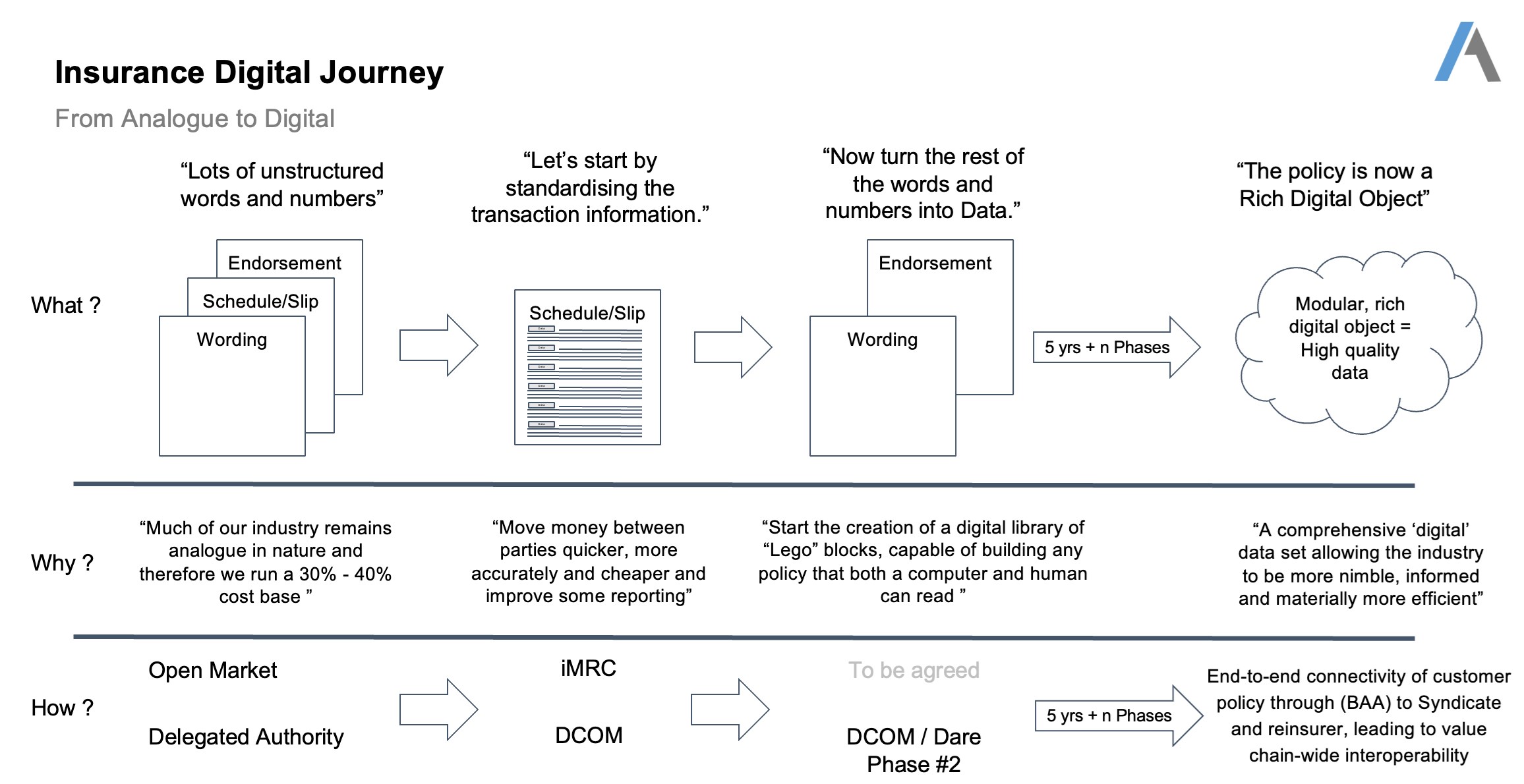

Today virtually all insurance contracts underwritten in the London Insurance Market are hand-crafted Word documents, which are then saved as PDFs and often still printed. This approach has provided the market with the flexibility to create bespoke coverage for our clients, but there are drawbacks. The iMRC hopes to begin to tackle this head on in a series of manageable stages.

Firstly, to the current drawbacks. These vary depending on your perspective:

From a Client’s perspective: Speed is the key delivery for the Client, whether that is speed of claim settlement, speed of documentation, speed of access to market etc. With documents often manually produced, speed is often slow across all these areas. This can lead to misinterpretation of data items by downstream processing, which then causes delays in Claim agreement and premium settlement.

From a Broker’s perspective: The advent of the original MRC went a long way to improving the Client service, as well as providing standardised documentation that assisted the Central Accounting services. However, this level of data ingested by the Central Service remain largely manual and prone to confusion, which is primarily caused by interpretation of language.

From a Carrier’s perspective: Extracting data from contracts is a labour intensive, expensive and time-consuming process. Until recent advancements in technology, contracts could not be consistently read and understood by machines, limiting their ability to take advantage of automation including portfolio analysis, but also leading to reconciliation and error rates between contract data and premium processing messages (which also adds more expense).

For Central Accounting: The current rejection rate is between 25% and 33%. It takes an average of 4.5 days, a process which involves thousands of people across the market, to produce a technical account from the analogue information submitted, as all data is manually entered - including some from faxes!!

So, what does the future look like and what role does the iMRC play?

The ultimate future vision is a fully computable contract. Computable contracting is a set of approaches that enable contracts to be built as digital objects, with significantly greater levels of in-built structure and logic, and represented in a way that is understandable (and usable) by humans and computers. As such, computable contracting represents an important shift in thinking, as well as an opportunity to develop the foundations upon which the insurance industry is built.

This vision is one where we are no longer trying to extract and interpret data out of documents, because the document is the data.

This future vision is akin to moving from Vinyl to Streaming, and there will be intermediate steps along the way. We will digitise every number and every word in the contract, resulting in instant contract production and data capture into downstream systems, including accounting and settlement. It means that “documents” are the human readable output from the process, not the start point (it might look and feel like a document, but it will be a series of digital objects). Today we start with documents and then expend untold sums trying to exact the data. The future is the other way round.

© Axiome Partners.

If that is the ultimate goal, so what are the steps towards that goal?

Firstly, we needed to define the core data that is needed to drive our processes within central services. That is known as the Core Data Record, or CDR (the Data Council approved the latest iteration of the CDR, which is aligned to ACORD standards, on 22 March 2022).

Secondly, we need to define who, when and how that CDR should flow between the parties to the contract. This is our process, roles and responsibilities workstream within the LMG’s Data Council.

Finally, we need to work out how to reliably structure the data in the contracts themselves. This is where the iMRC comes in.

The first step on the iMRC journey is the updated MRC guidance, which will:

1. Specify all the data that is needed downstream. The current guidance is silent on a good proportion of the CDR meaning that downstream systems simply have no chance of extracting data that is missing.

2. The second part of the iMRC is being far more specific as to how certain data elements should be represented. How should a date field be displayed for example? How should Sections be represented?

It is important to note that we are not proposing that all contracts conform to any one specific format. That will be left to individual firms, but firms will be required to include the essential data and include that data in a prescribed format.

All the CDR elements within the iMRC will map to the ACORD Global Reinsurance & Large Commercial data standards and that mapping work is ongoing. There is additional data that forms part of the CDR that is not in the new iMRC, such as the presentation of schedules of values.

The next step: This will be going beyond the CDR data fields into all remaining data fields and include the clauses, and then once we have the market trading data first, the age of MS Word as the mechanism for creating insurance contracts will finally come to an end and the significant cost savings and benefits of digitisation will be realised.

If you have questions about the iMRC, take a look at the LMG website or get in touch with iMRC@lloyds.com.

Written by Atrium's Justin Emrich, Chief Information Officer.